GBS Health Benefits Compliance

Medicare Secondary Payer (MSP) Rules:

Guardrails When Communicating with Medicare-Eligible Employees

Quick Summary

Under the Medicare Secondary Payer (MSP) rules, a group health plan (GHP) is generally required to pay first—and Medicare pays only what remains—whenever an employee or covered family member is eligible for both sources of coverage. MSP protection applies in three circumstances: when a person becomes entitled to Medicare because of age (65 or older), disability, or End-Stage Renal Disease (ESRD). By putting primary payment responsibility on the employer plan (subject to certain employer-size thresholds for age and disability, and a 30-month coordination period for ESRD), the MSP statute preserves Medicare’s resources while assuring employees and their dependents full access to the benefits promised under the GHP. Consequently, employers must structure plan terms, enrollment processes, and communications so they neither discourage Medicare-eligible individuals from staying on the GHP nor provide incentives to shift costs to Medicare—while still giving those individuals clear, neutral information about how the two coverages interact and what choices are available.

Medicare Secondary Payer (MSP) Rules

When an individual is enrolled in or eligible for both Medicare and their employer’s group health plan, the group health plan is usually the primary payer on claims and Medicare is the secondary payer. These coordination of benefits rules generally apply to individuals in “current employment status” and to their spouses and family members. Thus, for individuals who have both Medicare and retiree or COBRA coverage, the group health plan is NOT the primary payer because these benefits are not based on “current” employment status. However, for the third category above (ESRD), Medicare pays secondary for the first 30 months of ESRD coverage even if the individual is not in “current employment status.”

There are three reasons an individual could be enrolled in (or eligible for) Medicare: Age (age 65+), disability, or End-Stage Renal Disease (ESRD).

Employer size determines which MSP rules apply.

- Age. Employers with 20 or more employees must comply with the MSP rules for individuals who are Medicare-eligible based on age, which is 65 or older.

- Disability. Employers with 100 or more employees also must comply with the MSP rules for individuals of any age who are Medicare-eligible based on disability. (Note that this category will likely be dependents of active employees who have group health coverage available based on the employee’s current employment.)

- ESRD. Employers with 1 or more employees must comply with MSP rules for individuals who are Medicare-eligible based on End-Stage Renal Disease (ESRD) but only for the first 30 months of eligibility or entitlement to Medicare.

Employer Responsibilities

When the MSP rules apply to an employer, that organization must ensure the group health plans (GHPs) it sponsors are compliant with the following:

- Identifying Medicare eligible employees and individuals to whom the MSP rules apply

- Confirming the insurer/TPA sends quarterly Section 111 reports to the Centers for Medicare and Medicaid Services (CMS) listing Medicare-eligible individuals

- Ensuring the group health plan pays primary on claims for Medicare-eligible participants, where applicable (and not suggesting providers bill Medicare first if the GHP is primary)

- Ensuring there is no discrimination against employees and family members through actions or communications that would “take into account” or “differentiate” within the benefits it provides.

Discrimination under MSP Rules

It is important for employers that sponsor group health plans to understand the specifics within MSP rules in order to prevent discrimination. In practice, it can sometimes be tricky for employers to navigate. Although nuances can arise, the rule explicitly prohibits incentives at 42 CFR §411.103:

- An employer or other entity (for example, an insurer) is prohibited from offering Medicare beneficiaries financial or other benefits as incentives not to enroll in, or to terminate enrollment in, a GHP that is, or would be, primary to Medicare.

- An example the rule provides is offering to Medicare beneficiaries an alternative to the employer primary plan (for example, coverage of prescription drugs). The exception to that situation would be where the beneficiary has primary coverage other than Medicare, for example, primary coverage through their spouse’s employer.

42 CFR § 411.108 clarifies as well by providing examples of (prohibited) actions that constitute “taking into account” entitlement to Medicare. For more, see last section below. Also, the CMS MSP manual (at page12) provides more clarification about certain plans: Employers may not sponsor or contribute to individual Medigap or Medicare supplement policies for beneficiaries who have or whose spouse has current employment status [because these plans are secondary to Medicare].

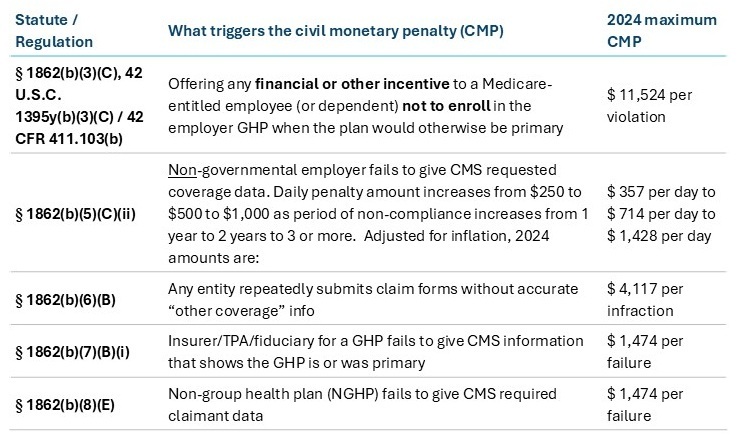

MSP Penalties

Failure to comply with MSP rules can result in civil penalties, reimbursement of Medicare for improper payments, and excise tax penalties.

Section 111 Late Reporting Penalties (not tiered for GHP RREs)

Applicable October 11, 2024, will be enforced as of October 11, 2025

Exposure to Double Damages

Apart from the fixed civil monetary penalties (CMPs) above, § 1862(b)(3)(A) lets Medicare (or a private plaintiff) sue and recover double the amount Medicare paid when a primary payer fails to pay. This is not capped and can dwarf the CMPs.

How to Avoid Compliance Issues and Penalties

Because the MSP rules have nuances that can sometimes be tricky for employers to navigate, this section provides numerous real-world examples of both permitted and prohibited communications, actions and practices by employers.

Examples of Permitted Communications and Actions

Examples of Permitted Communications and Actions

Employers may explain the basics of how Medicare coordinates with group health coverage. For example, it can explain that when an employee is enrolled in both the group health plan and Medicare, the group plan pays first and Medicare pays second. Employers may also describe the potential consequences of delaying Medicare Part B or D if the individual later loses group coverage, provided that the explanation is neutral and factual.

Employers May Provide Neutral Medicare Educational Resources

While employers cannot recommend that an employee leave the group health plan for Medicare, they may provide factual, non-biased resources to educate individuals about their options. However, employers and HR teams should not advise employees on whether or when to enroll in Medicare. It is allowable to refer individuals to:

- www.Medicare.gov and 1-800-MEDICARE

- State Health Insurance Assistance Programs (SHIP) and SHIP counselors

- CMS publications like “Medicare and Other Health Benefits: Your Guide to Who Pays First”

MSP rules do not specifically address whether an employer can inform individuals that licensed insurance agents or brokers can help them decide whether to enroll in Medicare, nor do they address whether an employer can refer individuals to specific agents or brokers. Employers should be cautious about recommending that individuals enroll in specific Medicare policies and/or referring individuals to an agent or broker from whom the employer will receive a commission or other financial remuneration if the individual enrolls in a Medicare policy or Medicare supplement.

Employers Should Document Neutrality and Train Internal Teams

Employers should train HR and benefits personnel on MSP rules and the importance of avoiding discriminatory or noncompliant communications. Any third-party materials distributed to employees should be reviewed to ensure they are unbiased and educational in nature. Keeping a record of communications can help demonstrate compliance if ever reviewed by CMS.

Employers May Offer Cash-in-Lieu or Opt-Out Arrangements as long as Offered to All

If offering a cash incentive to employees who waive health coverage, that incentive must be made available on equal terms to all eligible employees — not just to Medicare-eligible individuals. Offering a financial incentive specifically to Medicare-eligible individuals to opt out of the group plan is a direct violation of MSP rules and can trigger penalties from CMS.

Examples of Prohibited Communications and Actions

Prohibited Employer Communications

The flip-side of permitted communications listed above include the

following prohibited communications:

- Suggesting Medicare is cheaper or more suitable than the group health plan

- This includes casual conversations or benefits materials that reference Medicare as a more cost-effective or preferable option.

- Providing misleading or incomplete information that would have the effect of inducing a Medicare-entitled individual to reject the employer plan

- For example, employers should not suggest or imply that Medicare is a better or more appropriate choice than the group plan.

- Offering cash waivers only to Medicare-eligible employees

- Advising employees to leave the group plan in favor of Medicare

›Providing non-neutral educational resources.

Prohibited Employer Actions

In addition to the employer common communication pitfalls, the MSP regulations include numerous examples of employer actions that impermissibly discriminate against individuals, i.e. actions that “take into account” entitlement to Medicare, including but not limited to:

- Failing to pay group health plan benefits primary to Medicare, or instructing providers or suppliers to bill Medicare first when an individual is entitled to Medicare, and not specifying that applies only if Medicare is primary;

- Offering coverage that is secondary to Medicare to individuals entitled to Medicare;

- Terminating health plan coverage because an individual enrolls in Medicare, except as permitted under COBRA;

- Imposing limitations on benefits for a Medicare-entitled individual that do not apply to others enrolled in the plan, such as providing less comprehensive health care coverage, excluding benefits, reducing benefits, charging higher deductibles or coinsurance, providing for lower annual or lifetime benefit limits, or providing more restrictive preexisting conditions limitations;

- Charging a Medicare-entitled individual higher premiums than others pay;

- Requiring a Medicare-entitled individual to wait longer for coverage to begin;

- Paying providers and suppliers less for services furnished to a Medicare beneficiary than for the same services furnished to other enrollees;

- Providing misleading or incomplete information that would have the effect of inducing a Medicare-entitled individual to reject the employer plan, thereby making Medicare the primary payer;

- Including in its health insurance cards, claims forms, or brochures distributed to beneficiaries, providers, and suppliers, instructions to bill Medicare first for services furnished to Medicare beneficiaries without stipulating that such action may be taken only when Medicare is the primary payer;

- Refusing to enroll an individual in a group health plan for whom Medicare would be the secondary payer.

August 2025

This document is not intended to be exhaustive, nor should any information be construed as tax or legal advice.